A Health Savings Account, or “HSA”, is a tax-advantaged account where you save money to pay qualified healthcare expenses, as defined by the IRS. An HSA is available only with a consumer-directed health plan like the CDHP with HSA. Qualified expenses include medical, prescription, dental and vision costs for yourself and your dependent(s) covered under the CDHP.

If you’re on the Asurion network, click here to watch some helpful videos about the Health Savings Account and Flexible Spending Accounts from Alight, our HSA and FSA administrator.

|

Individual Coverage |

Employee + Dependent(s) Coverage |

|

|---|---|---|

|

IRS Annual HSA Contribution Limit |

$4,400 |

$8,750 |

|

Matching Contributions from Asurion |

$0.50 match for every $1 contributed, up to $500 |

$0.50 match for every $1 contributed, up to $1,000 |

|

If you contribute … |

At least $1,000 |

At least $2,000 |

|

Asurion contributes … |

$500 |

$1,000 |

|

Maximum Election for Employee (to avoid exceeding the IRS’s Total Annual Contribution Limit) |

$3,900 |

$7,750 |

|

Maximum Election for Employee Age 55+ ($1,000 Catch-up Contribution) |

$4,900 |

$8,750 |

REMEMBER:

* Total is inclusive of employee contributions plus company-matching contributions from Asurion.

Your HSA is designed for the long game, whether you’re planning for a baby, managing ongoing health needs or preparing for retirement. With our new matching program, we’re helping you build financial security while you remain present in all of life’s moments.

Think of your HSA as an investment account for your health. Start planning for the future and appeal to your inner investor. This is money that grows for you, tax-free, through the magic of compound interest.

We describe an HSA as “triple tax-advantaged” because it saves you money on taxes in three ways.

1

are pre-tax (so your gross pay is lower for tax purposes, too)

2

accrues untaxed

The HSA has great tax advantages like a 401(k), in addition to the following features:

|

You earn interest Your account balance grows until you spend it |

Contribution |

|

Interest |

|

Interest on interest |

|

Rollover feature Your balance rolls over year-to-year with no “use it or lose it” rules |

HSA balance |

|

Change Jobs |

|

Retire |

|

Investment options HSA funds can be invested to grow your savings for the future, including retirement |

HSA funds |

|

Mutual funds |

|

Future savings |

And there’s another advantage of an HSA: you never lose it. The balance rolls over year to year, and you can even take it with you if you leave the company or retire.

1

to pay your deductible and coinsurance

2

for planned or unplanned future healthcare needs; the balance rolls over year to year

3

with interest or through investment options for use in retirement

A CDHP is a specially designed plan that puts you, as the consumer of healthcare, in the driver’s seat of how you choose and use your coverage. Check out this general comparison of healthcare options.

|

Preferred provider (PPO) |

High Deductible (CDHP) |

|

|---|---|---|

|

PREVENTIVE CARE COVERED 100%? |

|

|

|

HAS AN ANNUAL DEDUCTIBLE? |

|

|

|

HAS AN ANNUAL OUT-OF-POCKET MAXIMUM? |

|

|

|

OUT-OF-NETWORK COVERAGE? |

Usually; often at a higher |

Yes, but at a higher |

|

REQUIRES A COPAYMENT WHEN YOU SEE A PROVIDER? |

|

|

|

CAN USE A HEALTH SAVINGS ACCOUNT (HSA) TO PAY FOR CARE (DEDUCTIBLE AND COINSURANCE)? |

|

|

1

In a traditional PPO you pay a copayment to see a provider, whereas in the CDHP plan, you pay all of your cost of care out of pocket until you reach the deductible.

2

In our CDHP and PPO plans you pay 20% of your care in coinsurance after you meet the deductible (in-network). If you plan ahead to save money in your HSA per paycheck, you can be ready if high healthcare costs hit.

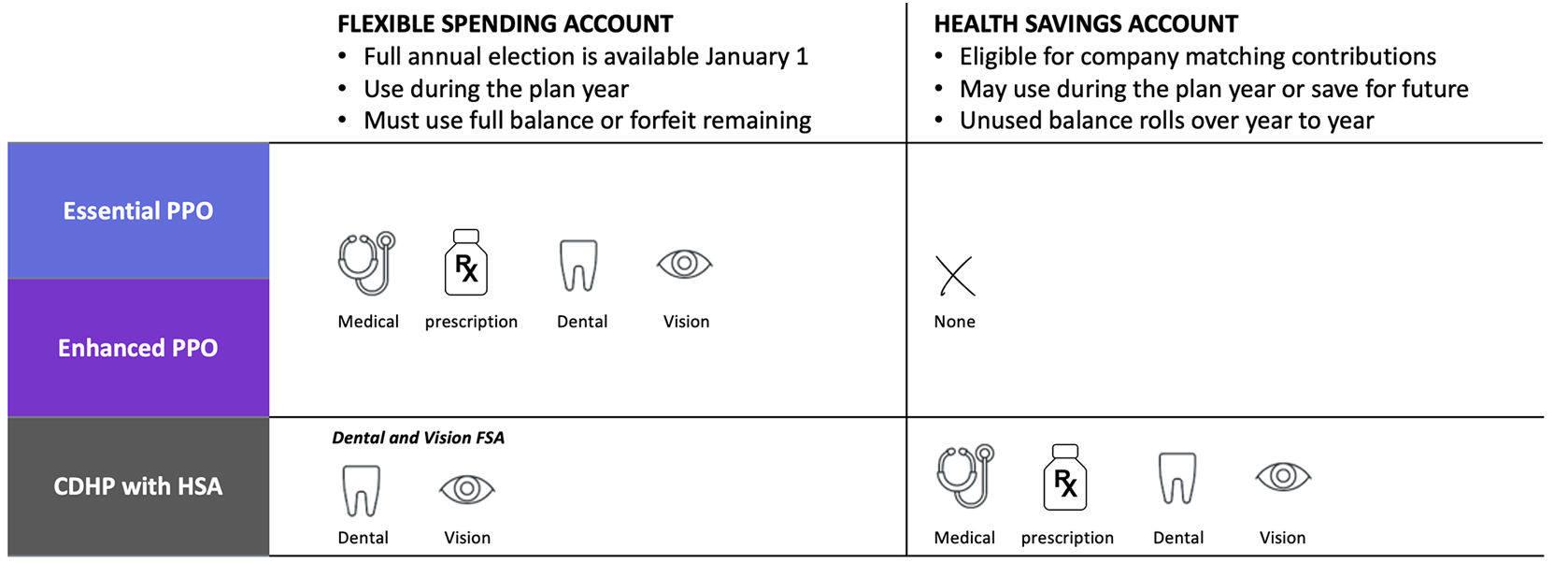

Sometimes all of these names and abbreviations might seem like alphabet soup. But Health Savings Accounts (HSAs) and Healthcare Flexible Spending Accounts (FSAs) are both important pre-tax savings accounts, and it’s worth understanding both of them. You may choose one or both — did you know they can work together?

You can contribute to both of these accounts on a pre-tax basis. But, bottom line, if you’d like to have an HSA, you must choose the United CDHP with HSA or Kaiser CDHP with HSA. A consumer-directed plan is the only plan type that meets the IRS’s qualification of being a high-deductible health plan (CDHP). If you choose the United CDHP with HSA or Kaiser CDHP with HSA, you may also open a Dental and Vision FSA — because you’ll use your HSA for medical and prescription expenses.

|

Health Savings Account |

Dental and Vision Flexible Spending Account |

|---|---|

|

Available to those who are enrolled in the CDHP with HSA, a high-deductible health plan — this is an IRS rule.

|

Available to those who are enrolled in a CDHP with HSA, a consumer-directed plan — this is an IRS rule.

|

|

Qualified expenses for the HSA include medical, prescription, dental and vision costs for yourself and your dependent(s) covered under the CDHP. |

Qualified expenses for the Dental and Vision FSA only include dental and vision costs for yourself and your covered dependent(s). |

As you can see, the HSA and FSA are a lot alike, but have key differences.

Keep these options in mind as you plan ahead for your healthcare needs.

Don’t let the opportunity to save pre-tax money pass you by!

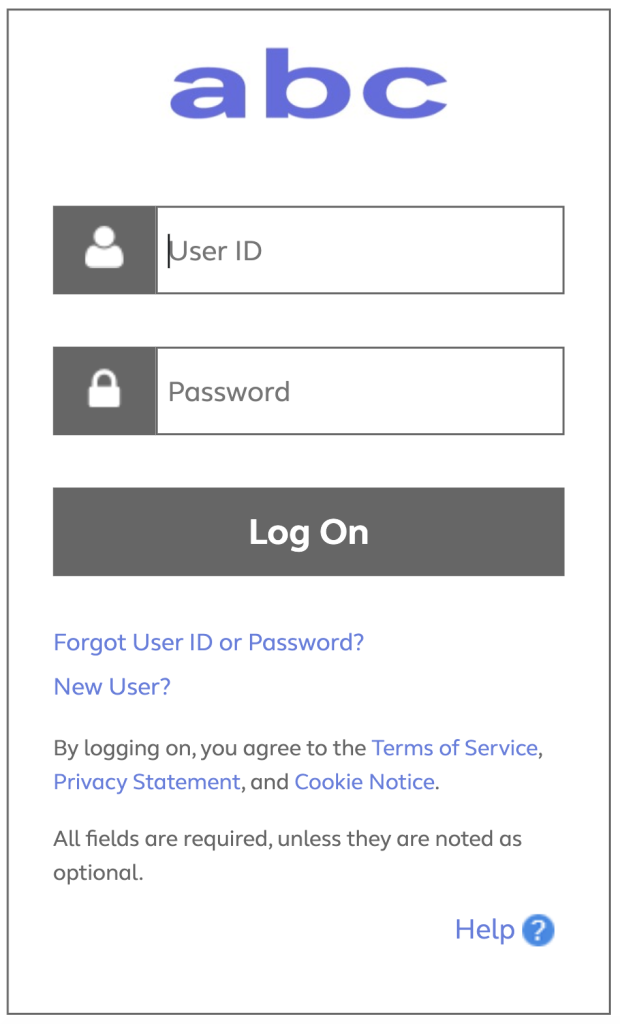

Heads up! You are leaving the ABC InfoShare. Unless you’re on the Asurion network, you’ll need your username and password to access Asurion Benefits Central at asurion.benefitsnow.com. Only current Asurion employees may log in.

If you don’t have the required log-in details, select Forgot User ID or Password? and follow the prompts. If this is your first visit to Asurion Benefits Central, click New User?

Questions: Call 844.968.6278.

Register in Asurion Learning for the meeting you’d like to attend. After registering, you’ll receive a confirmation email containing information about joining the meeting.

No events found.

Text “Benefits” to 67426 to have a link sent to your phone. Then, click the link to download the Alight Mobile app so you can access all the functions of the ABC on the go. (You’ll need to set your “Primary Phone” in Workday as your mobile number for full functionality.)